While China has received particular attention in the BEV (electric vehicle) market in recent years, significant changes are actually occurring in the Southeast Asian (ASEAN) market as well.

Currently reigning at the center of the market is VinFast, a newly born Vietnamese manufacturer.

The company’s overwhelming speed has allowed it to seize approximately 40% of the ASEAN market share.

However, behind the scenes, the reality is that the company is reporting a huge net loss of over $3 billion per year, and is running a deficit far in excess of its sales….

This time from various perspectives, including market dominance, vehicle models, battery supply chain, and financials,

We summarize its unique growth structure and the “Global South domination” behind it.

1. Tectonic shifts in the global BEV market and rapid growth of ASEAN

The global BEV market is currently at a major turning point.

While the Chinese and European markets are showing growth, growth in the U.S. has slowed down quickly due to policy changes by the Trump administration.

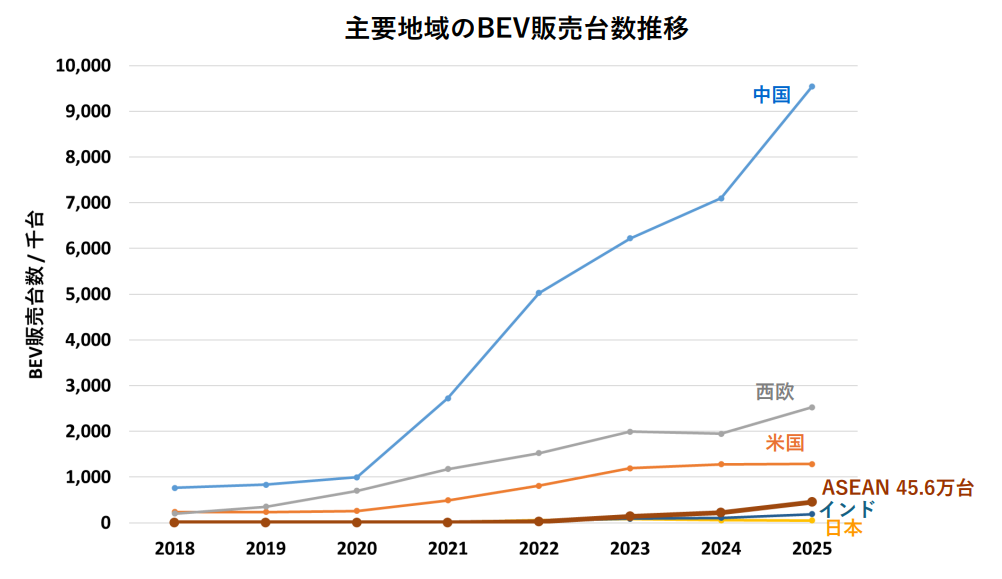

Under such circumstances, the ASEAN region is actually showing very high growth in the BEV market, although it has not received much attention in Japan.

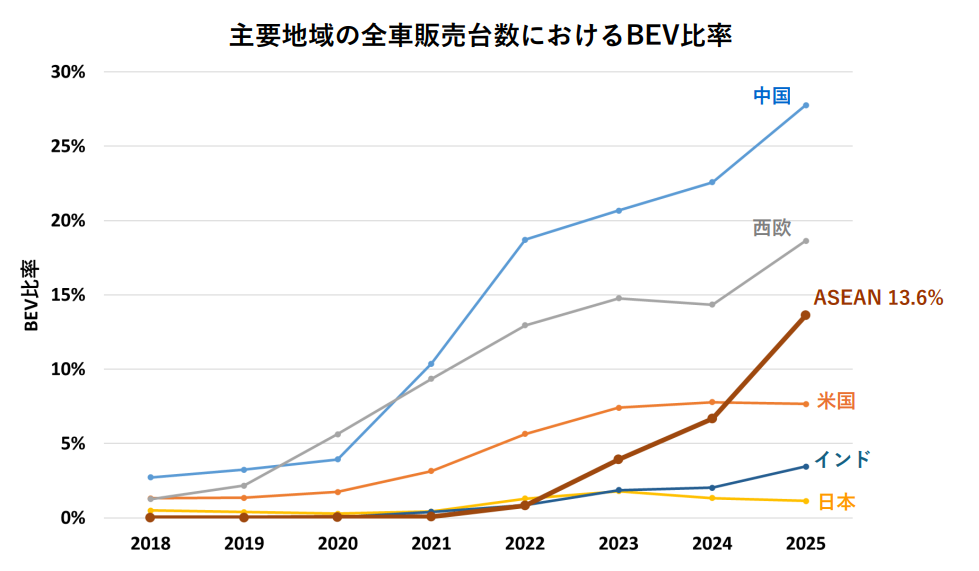

As shown in Figures 1 and 2, the BEV penetration rate in the ASEAN region has begun to show a significant growth curve after 2021.

The BEV ratio reached 13.6% in 2025, showing a penetration rate of “over 10%”, second only to China and Western Europe.

2. 40% ASEAN market share: VinFast’s dominant dominance and sales model

VinFast of Vietnam has been gaining significant market share in this ASEAN region.

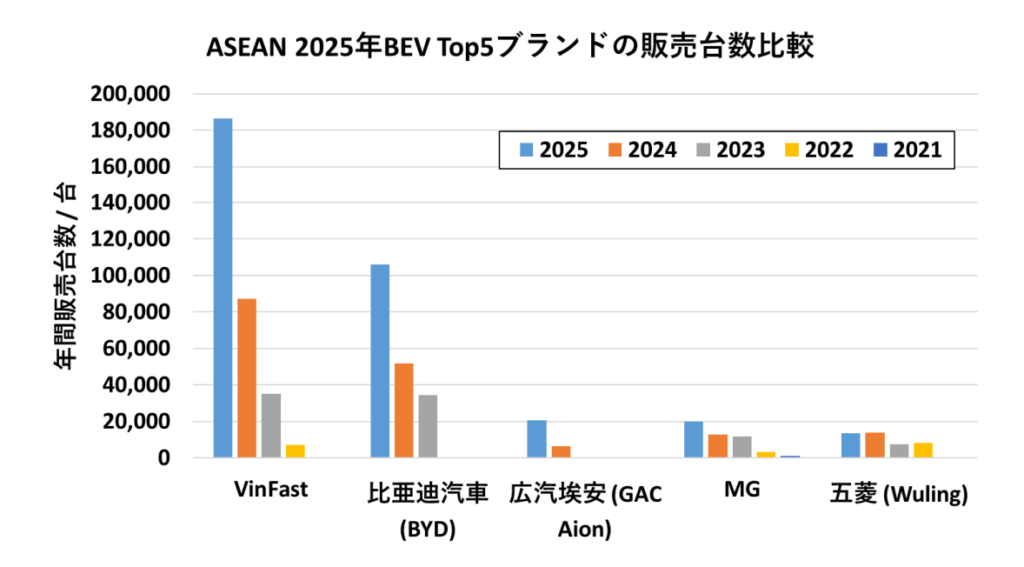

As shown in Figure 3, more than 180,000 units will be recorded in the ASEAN region in 2025.

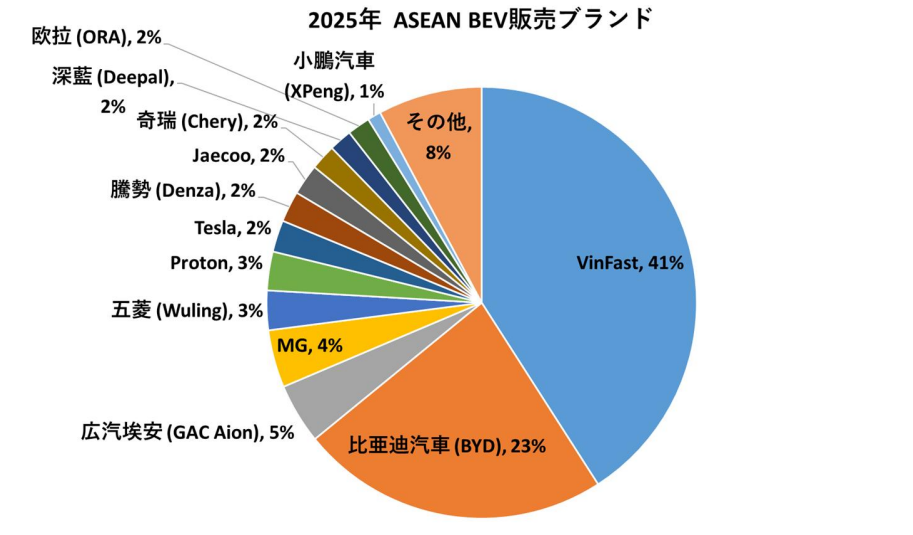

As shown in Figure 4, the company also recorded an astounding 41% share of BEV sales in the ASEAN region.

(This is not the main purpose of this article, but it can be seen that almost all of the BEVs are Chinese brands and none of them are Japanese brands…)

(Based on MARKLINES data)

(Based on MARKLINES data)

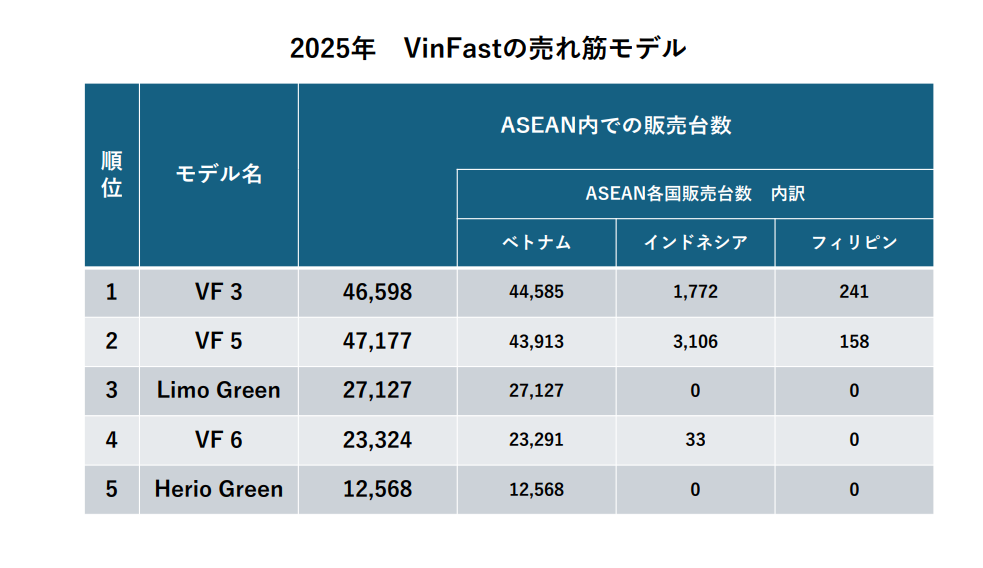

VinFast’s main models and specifications

And Figure 4 shows VinFast’s top 5 best-selling models in 2025.

In fact, VinFast is developing these mainstay models around a “battery subscription* ” that lowers the initial purchase cost.

*A unique fixed price service that sells and provides EV bodies and batteries separately.

The price of EV vehicles is kept low by adopting a subscription system in which battery lease fees are paid monthly.

We can also see that the main battleground for sales volume is still Vietnam.

(Based on MARKLINES data)

A summary of the top three selling models is shown below.

Both are small models in the low price range.

The source of this dominance, which puts the Chinese giant BYD far ahead, can be attributed to these lineup battles, which are optimized for the income and utility levels of emerging economies.

VF 3

A-segment equivalent mini-EV (Japanese kei car class).

Price 299 million VND~. (about 1,790,000 Japanese yen)

Battery capacity 18.64 kWh, cruising range 215 km (NEDC).

Fast charging takes about 36 minutes for 10~70% charge.

VF 5

Compact MPV equivalent to A~B segment.

Price 499 million VND.

Battery capacity 37.23 kWh, cruising range 300 km (NEDC).

Quick charge up to 80 kW. 10~70% charge in about 30 minutes.

Limo Green

A 7-seat mid-size MPV primarily for fleet and cab use.

Price 749 million VND.

Battery capacity 60.13 kWh, cruising range 450 km (NEDC).

Quick charge up to 80 kW. 10~70% charge in about 30 minutes.

“Infrastructure packages” as a barrier to entry

In addition to the above low-cost vehicles, 150,000 charging ports built through the company group’s charging service company , V-Green,

It serves as a strong barrier to entry (MOAT) for other brands.

https://vgreen.net/en/tram-sac-o-to-dien

In emerging countries where infrastructure is underdeveloped, a vertically integrated model that not only “sells cars” but also provides a “charging and service network” as a set,

It is a unique competitive advantage that is difficult for generic brands to imitate.

3. Establishment of a battery and vertically integrated supply chain

The core of VinFast’s cost competitiveness is also visible in the vertical integration of batteries through the group company VinES and the use of strategic partnerships.

- Strategic shift to LFP: Early high-end models used Samsung SDI (21700 NCA cells), but now, in order to optimize TCO (total cost of ownership) in the Global South, the shift to LFP (lithium iron phosphate) cells by Gotion High-Tech and CATL of China The shift to LFP (lithium iron phosphate) cells by Gotion High-Tech and CATL in China is becoming clearer.

https://www.catl.com/en/news/1034.html

- Promotion of local production: The LFP cell plant (5 GWh/year) built at the Ha Tinh Plant in Vietnam is the cornerstone of localization that maximizes tariff benefits while avoiding geopolitical risks.

“Forced Market Creation” Strategy

By pressing ahead with its own “car + battery + charging network,” the company is forcibly creating a market by controlling its own uncertain infrastructure environment unique to emerging markets.

This goes beyond being a mere manufacturer and demonstrates our ambition to be a “platformer” that defines the energy and transportation infrastructure of emerging economies.

4. The merits and demerits of “demand within the ecosystem” that supports the abnormal growth speed

An integral part of VinFast’s growth is Vingroup’s unique “I buy first, you buy later” strategy.

He said, “First, I (as the owner) take the risk of buying and investing to prove the quality. Customers can buy only after their value is recognized.”

This is a slogan or attitude that shows a strong commitment to the company’s brand.

In other words,

The manufacturer (me) will take the lead in assuring quality, and I hope that consumers will feel secure in following suit.

This will be a strategy for gaining trust that only an emerging manufacturer can demonstrate.

“Running ads” strategy based on own demand

For example, in 2023, more than 70% of sales were to GSM (Green and Smart Mobility), an electric cab company within the group.

We offer an extremely strong incentive to GSM drivers: “10% discount on vehicle price + 90% loan (3 years)” to force them to create initial demand.

- Ensure initial capacity utilization: Infrastructure (V-Green) capacity utilization is secured by cab demand.

- Exposure effect: By having a large number of EVs running in the city, a sense of security is created for general consumers (running advertisement).

A huge financial cost

However, this strategy entails a huge “hemorrhage”.

Net losses amounted to approximately $3.2 billion in 2024, compared to net sales of approximately $1.8 billion.

The “Revenue-to-Loss ratio” of approximately 1.8 times net sales indicates that the company is in an “ultra-high risk mode,” which is out of the norm for normal corporate management.

5. Analysis of the financial structure: “free compensation” by the founder and the logic of expansion

The gross margin in 2024 was an abysmal -57.4%.

Behind this lies strategic decision-making.

(Incidentally, Vingroup is able to do this because it earns a lot of revenue from its real estate business, Vinhomes.)

https://vinfastauto.com/vn_en/vinfast-reports-fourth-quarter-and-full-year-2024-financial-results

Special capital structure and “compensating” identity

- Factors contributing to the gross profit deficit: in addition to sales promotion expenses, the cost of the “free recharge program,” which amounted to approximately $243 million in 2024 alone, was recorded as a sales deduction.

This is interpreted as a “strategic cost” to capture market share rather than an operational inefficiency. - Founder Dependence: A grant of up to $2 billion from founder Pham Nhat Vuong and a loan of approximately $1.2 billion from Vingroup support the business.

strategic intent

The reason for the rush to expand market share, even without regard to short-term PL (profit/loss), is to standardize the “EV, infrastructure, finance, and mobility” package in Vietnam,

This is because we are pursuing a long-term option value to export it as a “proven model” to the Global South.

6. Future outlook: break-even in 2026 and exports to the Global South

VinFast has set an official goal of “break-even by the end of 2026 “.

However, based on the current free charging policy and sales incentive levels, this is very difficult to achieve in reality.

Assumptions and gaps necessary to turn a profit

The company and its founders “aim to break-even by the end of 2026 with $3.5 billion in support,” assuming

(1) Sales in excess of 200,000 units per year, (2) Significant reduction of manufacturing costs, (3) Reduction of promotional and free-of-charge measures

The following is a list of

However, based on a gross margin of minus 57% and a final deficit of approximately $3.2 billion for full year 2024, and a gross margin of minus 40% and a quarterly deficit of $810 million for Q2 2025, dramatic improvement in gross margin and SG&A structure is needed to return to profitability by 2014, and the gap is expected to be large.

If free recharges and discounts continue

Free recharging alone is expected to generate sales deductions equivalent to about $240 million in 2024, and costs are expected to grow even more at this rate as the number of vehicles increases.

Vietnam has committed to free until the end of June 2027.

However, even in 2026, recharge revenues in major markets will not stand, and profitability must be achieved only by “vehicle margin improvement + promo compression + economies of scale”,

The hurdle is seen as quite high.

https://www.edisongroup.com/research/scaling-up-for-regional-ev-adoption/BM-2368

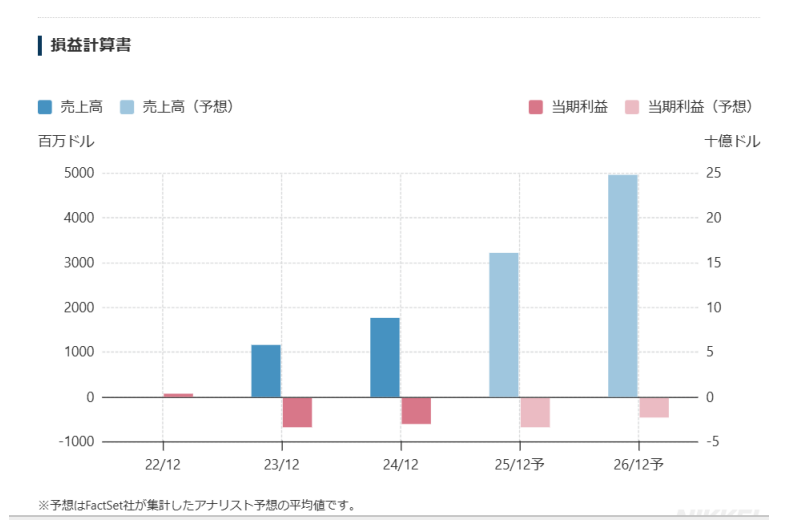

For reference, below is the current status of VinFast’s PL (income statement) and future projections by Nikkei Shimbun.

It indicates that even at the end of 2026, net income is expected to be a loss of approximately $2 billion or more.

https://www.nikkei.com/nkd/company/us/VFS/finance/

Also in many external analyst reports, including these,

The break even at the end of ’26 is a target for management and requires a very bullish premise to realize.”

The current situation is that the company is expected to fail to achieve the sales plan and that a delay of several years is possible depending on price competition.

We’ll see what happens….

Summary: A Litmus Test for Global Mobility Hegemony

This is a summary of our focus on VinFast, which is showing rapid growth in the ASEAN market.

While attention in Japan is still limited, VinFast will measure “whether BEVs can be a self-sustaining business in emerging countries,

I think it can be seen as an important and demanding real-time testing ground for the world.

If their export model of integrating “car + infrastructure + finance + mobility services” is successful,

Chinese manufacturers that rely on inexpensive vehicle sales (although the excessive price war will be rectified to some extent in the future…) and,

There may even be a possibility of surpassing existing manufacturers who are lagging behind in the EV shift.

This may be a bit of an exaggeration, but the success or failure of VinFast will be very interesting in terms of determining the future dominance of mobility in the world, especially in the Global South.

We will continue to watch.

We will continue to publish commentary articles on electric vehicles and electrification from an objective perspective that is easy to understand for as many people as possible.

If you have any topics you would like us to cover, or if you have any comments regarding our commentary, we would appreciate your comments on our website or Linkedin.

・Our website: https://blueskyinc.co.jp/

・Linkedin: https://www.linkedin.com/company/blueskyinc/?viewAsMember=true

This article was written by.

SASAKI Yusuke

Manager, Blue Sky Technology Inc.